Construction Accounting and Financial Management Chapter 3 Solutions

|

12. Cost Control, Monitoring and Accounting

12.1 The Cost Control Problem

During the execution of a project, procedures for project control and record keeping become indispensable tools to managers and other participants in the construction process. These tools serve the dual purpose of recording the financial transactions that occur as well as giving managers an indication of the progress and problems associated with a project. The problems of project control are aptly summed up in an old definition of a project as "any collection of vaguely related activities that are ninety percent complete, over budget and late." [1] The task of project control systems is to give a fair indication of the existence and the extent of such problems.

In this chapter, we consider the problems associated with resource utilization, accounting, monitoring and control during a project. In this discussion, we emphasize the project management uses of accounting information. Interpretation of project accounts is generally not straightforward until a project is completed, and then it is too late to influence project management. Even after completion of a project, the accounting results may be confusing. Hence, managers need to know how to interpret accounting information for the purpose of project management. In the process of considering management problems, however, we shall discuss some of the common accounting systems and conventions, although our purpose is not to provide a comprehensive survey of accounting procedures.

The limited objective of project control deserves emphasis. Project control procedures are primarily intended to identify deviations from the project plan rather than to suggest possible areas for cost savings. This characteristic reflects the advanced stage at which project control becomes important. The time at which major cost savings can be achieved is during planning and design for the project. During the actual construction, changes are likely to delay the project and lead to inordinate cost increases. As a result, the focus of project control is on fulfilling the original design plans or indicating deviations from these plans, rather than on searching for significant improvements and cost savings. It is only when a rescue operation is required that major changes will normally occur in the construction plan.

Finally, the issues associated with integration of information will require some discussion. Project management activities and functional concerns are intimately linked, yet the techniques used in many instances do not facilitate comprehensive or integrated consideration of project activities. For example, schedule information and cost accounts are usually kept separately. As a result, project managers themselves must synthesize a comprehensive view from the different reports on the project plus their own field observations. In particular, managers are often forced to infer the cost impacts of schedule changes, rather than being provided with aids for this process. Communication or integration of various types of information can serve a number of useful purposes, although it does require special attention in the establishment of project control procedures.

Back to top12.2 The Project Budget

For cost control on a project, the construction plan and the associated cash flow estimates can provide the baseline reference for subsequent project monitoring and control. For schedules, progress on individual activities and the achievement of milestone completions can be compared with the project schedule to monitor the progress of activities. Contract and job specifications provide the criteria by which to assess and assure the required quality of construction. The final or detailed cost estimate provides a baseline for the assessment of financial performance during the project. To the extent that costs are within the detailed cost estimate, then the project is thought to be under financial control. Overruns in particular cost categories signal the possibility of problems and give an indication of exactly what problems are being encountered. Expense oriented construction planning and control focuses upon the categories included in the final cost estimation. This focus is particular relevant for projects with few activities and considerable repetition such as grading and paving roadways.

For control and monitoring purposes, the original detailed cost estimate is typically converted to a project budget, and the project budget is used subsequently as a guide for management. Specific items in the detailed cost estimate become job cost elements. Expenses incurred during the course of a project are recorded in specific job cost accounts to be compared with the original cost estimates in each category. Thus, individual job cost accounts generally represent the basic unit for cost control. Alternatively, job cost accounts may be disaggregated or divided into work elements which are related both to particular scheduled activities and to particular cost accounts. Work element divisions will be described in Section 12.8.

In addition to cost amounts, information on material quantities and labor inputs within each job account is also typically retained in the project budget. With this information, actual materials usage and labor employed can be compared to the expected requirements. As a result, cost overruns or savings on particular items can be identified as due to changes in unit prices, labor productivity or in the amount of material consumed.

The number of cost accounts associated with a particular project can vary considerably. For constructors, on the order of four hundred separate cost accounts might be used on a small project. [2] These accounts record all the transactions associated with a project. Thus, separate accounts might exist for different types of materials, equipment use, payroll, project office, etc. Both physical and non-physical resources are represented, including overhead items such as computer use or interest charges. Table 12-1 summarizes a typical set of cost accounts that might be used in building construction. [3] Note that this set of accounts is organized hierarchically, with seven major divisions (accounts 201 to 207) and numerous sub-divisions under each division. This hierarchical structure facilitates aggregation of costs into pre-defined categories; for example, costs associated with the superstructure (account 204) would be the sum of the underlying subdivisions (ie. 204.1, 204.2, etc.) or finer levels of detail (204.61, 204.62, etc.). The sub-division accounts in Table 12-1 could be further divided into personnel, material and other resource costs for the purpose of financial accounting, as described in Section 12.4.

| 201 | Clearing and Preparing Site |

202202.1 | SubstructureExcavation and Shoring |

| 203 | Outside Utilities (water, gas, sewer, etc.) |

204204.1 | SuperstructureMasonry Construction |

| 205 | Paving, Curbs, Walks |

| 206 | Installed Equipment (elevators, revolving doors, mailchutes, etc.) |

| 207 | Fencing |

In developing or implementing a system of cost accounts, an appropriate numbering or coding system is essential to facilitate communication of information and proper aggregation of cost information. Particular cost accounts are used to indicate the expenditures associated with specific projects and to indicate the expenditures on particular items throughout an organization. These are examples of different perspectives on the same information, in which the same information may be summarized in different ways for specific purposes. Thus, more than one aggregation of the cost information and more than one application program can use a particular cost account. Separate identifiers of the type of cost account and the specific project must be provided for project cost accounts or for financial transactions. As a result, a standard set of cost codes such as the MASTERFORMAT codes described in Chapter 9 may be adopted to identify cost accounts along with project identifiers and extensions to indicate organization or job specific needs. Similarly the use of databases or, at a minimum, inter-communicating applications programs facilitate access to cost information, as described in Chapter 14.

Converting a final cost estimate into a project budget compatible with an organization's cost accounts is not always a straightforward task. As described in Chapter 5, cost estimates are generally disaggregated into appropriate functional or resource based project categories. For example, labor and material quantities might be included for each of several physical components of a project. For cost accounting purposes, labor and material quantities are aggregated by type no matter for which physical component they are employed. For example, particular types of workers or materials might be used on numerous different physical components of a facility. Moreover, the categories of cost accounts established within an organization may bear little resemblance to the quantities included in a final cost estimate. This is particularly true when final cost estimates are prepared in accordance with an external reporting requirement rather than in view of the existing cost accounts within an organization.

One particular problem in forming a project budget in terms of cost accounts is the treatment of contingency amounts. These allowances are included in project cost estimates to accommodate unforeseen events and the resulting costs. However, in advance of project completion, the source of contingency expenses is not known. Realistically, a budget accounting item for contingency allowance should be established whenever a contingency amount was included in the final cost estimate.

A second problem in forming a project budget is the treatment of inflation. Typically, final cost estimates are formed in terms of real dollars and an item reflecting inflation costs is added on as a percentage or lump sum. This inflation allowance would then be allocated to individual cost items in relation to the actual expected inflation over the period for which costs will be incurred.

Example 12-1: Project Budget for a Design Office

An example of a small project budget is shown in Table 12-2. This budget might be used by a design firm for a specific design project. While this budget might represent all the work for this firm on the project, numerous other organizations would be involved with their own budgets. In Table 12-2, a summary budget is shown as well as a detailed listing of costs for individuals in the Engineering Division. For the purpose of consistency with cost accounts and managerial control, labor costs are aggregated into three groups: the engineering, architectural and environmental divisions. The detailed budget shown in Table 12-2 applies only to the engineering division labor; other detailed budgets amounts for categories such as supplies and the other work divisions would also be prepared. Note that the salary costs associated with individuals are aggregated to obtain the total labor costs in the engineering group for the project. To perform this aggregation, some means of identifying individuals within organizational groups is required. Accompanying a budget of this nature, some estimate of the actual man-hours of labor required by project task would also be prepared. Finally, this budget might be used for internal purposes alone. In submitting financial bills and reports to the client, overhead and contingency amounts might be combined with the direct labor costs to establish an aggregate billing rate per hour. In this case, the overhead, contingency and profit would represent allocated costs based on the direct labor costs.

| Personnel Architectural Division Engineering Environmental Division Total Other Direct Expenses Overhead Contingency and Profit Total | $ 67,251.00 45,372.00 28,235.00 $140,858.00 2,400.00 $ 5,700.00 $ 175,869.60 $ 95,700.00$ 418,127.60 |

| Senior Engineer Associate Engineer Engineer Technician Total | $ 11,562.00 21,365.00 12,654.00 $ 45,372.00 |

Example 12-2: Project Budget for a Constructor

Table 12-3 illustrates a summary budget for a constructor. This budget is developed from a project to construct a wharf. As with the example design office budget above, costs are divided into direct and indirect expenses. Within direct costs, expenses are divided into material, subcontract, temporary work and machinery costs. This budget indicates aggregate amounts for the various categories. Cost details associated with particular cost accounts would supplement and support the aggregate budget shown in Table 12-3. A profit and a contingency amount might be added to the basic budget of $1,715,147 shown in Table 12-3 for completeness.

| Material Cost | Subcontract Work | Temporary Work | Machinery Cost | Total Cost | |

| Steel Piling Tie-rod Anchor-Wall Backfill Coping Dredging Fender Other Sub-total | $292,172 88,233 130,281 242,230 42,880 0 48,996 5,000 $849,800 | $129,178 29,254 60,873 27,919 22,307 111,650 10,344 32,250 $423,775 | $16,389 0 0 0 13,171 0 0 0 $29,560 | $0 0 0 0 0 0 1,750 0 $1,750 | $437,739 117,487 191,154 300,149 78,358 111,650 61,090 37,250 $1,304,885 |

| Summary Total of direct cost Indirect Cost Common Temporary Work Common Machinery Transportation Office Operating Costs Total of Indirect Cost Total Project Cost |

| ||||

Back to top

12.3 Forecasting for Activity Cost Control

For the purpose of project management and control, it is not sufficient to consider only the past record of costs and revenues incurred in a project. Good managers should focus upon future revenues, future costs and technical problems. For this purpose, traditional financial accounting schemes are not adequate to reflect the dynamic nature of a project. Accounts typically focus on recording routine costs and past expenditures associated with activities. [4] Generally, past expenditures represent sunk costs that cannot be altered in the future and may or may not be relevant in the future. For example, after the completion of some activity, it may be discovered that some quality flaw renders the work useless. Unfortunately, the resources expended on the flawed construction will generally be sunk and cannot be recovered for re-construction (although it may be possible to change the burden of who pays for these resources by financial withholding or charges; owners will typically attempt to have constructors or designers pay for changes due to quality flaws). Since financial accounts are historical in nature, some means of forecasting or projecting the future course of a project is essential for management control. In this section, some methods for cost control and simple forecasts are described.

An example of forecasting used to assess the project status is shown in Table 12-4. In this example, costs are reported in five categories, representing the sum of all the various cost accounts associated with each category:

- Budgeted Cost

The budgeted cost is derived from the detailed cost estimate prepared at the start of the project. Examples of project budgets were presented in Section 12.2. The factors of cost would be referenced by cost account and by a prose description. - Estimated total cost

The estimated or forecast total cost in each category is the current best estimate of costs based on progress and any changes since the budget was formed. Estimated total costs are the sum of cost to date, commitments and exposure. Methods for estimating total costs are described below. - Cost Committed and Cost Exposure!! Estimated cost to completion in each category in divided into firm commitments and estimated additional cost or exposure. Commitments may represent material orders or subcontracts for which firm dollar amounts have been committed.

- Cost to Date

The actual cost incurred to date is recorded in column 6 and can be derived from the financial record keeping accounts. - Over or (Under)

A final column in Table 12-4 indicates the amount over or under the budget for each category. This column is an indicator of the extent of variance from the project budget; items with unusually large overruns would represent a particular managerial concern. Note that variance is used in the terminology of project control to indicate a difference between budgeted and actual expenditures. The term is defined and used quite differently in statistics or mathematical analysis. In Table 12-4, labor costs are running higher than expected, whereas subcontracts are less than expected.

The current status of the project is a forecast budget overrun of $5,950. with 23 percent of the budgeted project costs incurred to date.

| Factor | Budgeted Cost | Estimated Total Cost | Cost Committed | Cost Exposure | Cost To Date | Over or (Under) |

| Labor Material Subcontracts Equipment Other Total | $99,406 88,499 198,458 37,543 72,693 496,509 | $102,342 88,499 196,323 37,543 81,432 506,139 | $49,596 42,506 83,352 23,623 49,356 248,433 | --- 45,993 97,832 --- --- 143,825 | $52,746 --- 15,139 13,920 32,076 113,881 | $2,936 0 (2,135) 0 8,739 5,950 |

For project control, managers would focus particular attention on items indicating substantial deviation from budgeted amounts. In particular, the cost overruns in the labor and in the "other expense category would be worthy of attention by a project manager in Table 12-4. A next step would be to look in greater detail at the various components of these categories. Overruns in cost might be due to lower than expected productivity, higher than expected wage rates, higher than expected material costs, or other factors. Even further, low productivity might be caused by inadequate training, lack of required resources such as equipment or tools, or inordinate amounts of re-work to correct quality problems. Review of a job status report is only the first step in project control.

The job status report illustrated in Table 12-4 employs explicit estimates of ultimate cost in each category of expense. These estimates are used to identify the actual progress and status of a expense category. Estimates might be made from simple linear extrapolations of the productivity or cost of the work to date on each project item. Algebraically, a linear estimation formula is generally one of two forms. Using a linear extrapolation of costs, the forecast total cost, Cf , is:

| (12.1) |  |

where Ct is the cost incurred to time t and pt is the proportion of the activity completed at time t. For example, an activity which is 50 percent complete with a cost of $40,000 would be estimated to have a total cost of $40,000/0.5 = $80,000. More elaborate methods of forecasting costs would disaggregate costs into different categories, with the total cost the sum of the forecast costs in each category.

Alternatively, the use of measured unit cost amounts can be used for forecasting total cost. The basic formula for forecasting cost from unit costs is:

| (12.2) |  |

where Cf is the forecast total cost, W is the total units of work, and ct is the average cost per unit of work experienced up to time t. If the average unit cost is $50 per unit of work on a particular activity and 1,600 units of work exist, then the expected cost is (1,600)(50) = $80,000 for completion.

The unit cost in Equation (12.2) may be replaced with the hourly productivity and the unit cost per hour (or other appropriate time period), resulting in the equation:

| (12.3) |  |

where the cost per work unit (ct) is replaced by the time per unit, ht, divided by the cost per unit of time, ut.

More elaborate forecasting systems might recognize peculiar problems associated with work on particular items and modify these simple proportional cost estimates. For example, if productivity is improving as workers and managers become more familiar with the project activities, the estimate of total costs for an item might be revised downward. In this case, the estimating equation would become:

| (12.4) |  |

where forecast total cost, Cf, is the sum of cost incurred to date, Ct, and the cost resulting from the remaining work (W - Wt) multiplied by the expected cost per unit time period for the remainder of the activity, ct.

As a numerical example, suppose that the average unit cost has been $50 per unit of work, but the most recent figure during a project is $45 per unit of work. If the project manager was assured that the improved productivity could be maintained for the remainder of the project (consisting of 800 units of work out of a total of 1600 units of work), the cost estimate would be (50)(800) + (45)(800) = $76,000 for completion of the activity. Note that this forecast uses the actual average productivity achieved on the first 800 units and uses a forecast of productivity for the remaining work. Historical changes in productivity might also be used to represent this type of non-linear changes in work productivity on particular activities over time.

In addition to changes in productivities, other components of the estimating formula can be adjusted or more detailed estimates substituted. For example, the change in unit prices due to new labor contracts or material supplier's prices might be reflected in estimating future expenditures. In essence, the same problems encountered in preparing the detailed cost estimate are faced in the process of preparing exposure estimates, although the number and extent of uncertainties in the project environment decline as work progresses. The only exception to this rule is the danger of quality problems in completed work which would require re-construction.

Each of the estimating methods described above require current information on the state of work accomplishment for particular activities. There are several possible methods to develop such estimates, including [5]:

- Units of Work Completed

For easily measured quantities the actual proportion of completed work amounts can be measured. For example, the linear feet of piping installed can be compared to the required amount of piping to estimate the percentage of piping work completed. - Incremental Milestones

Particular activities can be sub-divided or "decomposed" into a series of milestones, and the milestones can be used to indicate the percentage of work complete based on historical averages. For example, the work effort involved with installation of standard piping might be divided into four milestones:- Spool in place: 20% of work and 20% of cumulative work.

- Ends welded: 40% of work and 60% of cumulative work.

- Hangars and Trim Complete: 30% of work and 90% of cumulative work.

- Hydrotested and Complete: 10% of work and 100% of cumulative work.

Thus, a pipe section for which the ends have been welded would be reported as 60% complete.

- Opinion

Subjective judgments of the percentage complete can be prepared by inspectors, supervisors or project managers themselves. Clearly, this estimated technique can be biased by optimism, pessimism or inaccurate observations. Knowledgeable estimaters and adequate field observations are required to obtain sufficient accuracy with this method. - Cost Ratio

The cost incurred to date can also be used to estimate the work progress. For example, if an activity was budgeted to cost $20,000 and the cost incurred at a particular date was $10,000, then the estimated percentage complete under the cost ratio method would be 10,000/20,000 = 0.5 or fifty percent. This method provides no independent information on the actual percentage complete or any possible errors in the activity budget: the cost forecast will always be the budgeted amount. Consequently, managers must use the estimated costs to complete an activity derived from the cost ratio method with extreme caution.

Systematic application of these different estimating methods to the various project activities enables calculation of the percentage complete or the productivity estimates used in preparing job status reports.

In some cases, automated data acquisition for work accomplishments might be instituted. For example, transponders might be moved to the new work limits after each day's activity and the new locations automatically computed and compared with project plans. These measurements of actual progress should be stored in a central database and then processed for updating the project schedule. The use of database management systems in this fashion is described in Chapter 14.

Example 12-3: Estimated Total Cost to Complete an Activity

Suppose that we wish to estimate the total cost to complete piping construction activities on a project. The piping construction involves 1,000 linear feet of piping which has been divided into 50 sections for management convenience. At this time, 400 linear feet of piping has been installed at a cost of $40,000 and 500 man-hours of labor. The original budget estimate was $90,000 with a productivity of one foot per man-hour, a unit cost of $60 per man hour and a total material cost of $ 30,000. Firm commitments of material delivery for the $30,000 estimated cost have been received.The first task is to estimate the proportion of work completed. Two estimates are readily available. First, 400 linear feet of pipe is in place out of a total of 1000 linear feet, so the proportion of work completed is 400/1000 = 0.4 or 40%. This is the "units of work completed" estimation method. Second, the cost ratio method would estimate the work complete as the cost-to-date divided by the cost estimate or $40,000/$ 90,000 = 0.44 or 44%. Third, the "incremental milestones" method would be applied by examining each pipe section and estimating a percentage complete and then aggregating to determine the total percentage complete. For example, suppose the following quantities of piping fell into four categories of completeness:

hangars and trim complete (90%)

ends welded (60%)

spool in place (20%)

20 ft

5 ft

0 ftThen using the incremental milestones shown above, the estimate of completed work would be 380 + (20)(0.9) + (5)(0.6) + 0 = 401 ft and the proportion complete would be 401 ft/1,000 ft = 0.401 or 40% after rounding.

Once an estimate of work completed is available, then the estimated cost to complete the activity can be calculated. First, a simple linear extrapolation of cost results in an estimate of $40,000/0.4 = $100,000. for the piping construction using the 40% estimate of work completed. This estimate projects a cost overrun of 100,000 - 90,000 = $10,000.

Second, a linear extrapolation of productivity results in an estimate of (1000 ft.)(500 hrs/400 ft.)($60/hr) + 30,000 = $105,000. for completion of the piping construction. This estimate suggests a variance of 105,000 - 90,000 = $15,000 above the activity estimate. In making this estimate, labor and material costs entered separately, whereas the two were implicitly combined in the simple linear cost forecast above. The source of the variance can also be identified in this calculation: compared to the original estimate, the labor productivity is 1.25 hours per foot or 25% higher than the original estimate.

Example 12-4: Estimated Total Cost for Completion

The forecasting procedures described above assumed linear extrapolations of future costs, based either on the complete experience on the activity or the recent experience. For activities with good historical records, it can be the case that a typically non-linear profile of cost expenditures and completion proportions can be estimated. Figure 12-1 illustrates one possible non-linear relationships derived from experience in some particular activity. The progress on a new job can be compared to this historical record. For example, point A in Figure 12-1 suggests a higher expenditure than is normal for the completion proportion. This point represents 40% of work completed with an expenditure of 60% of the budget. Since the historical record suggests only 50% of the budget should be expended at time of 40% completion, a 60 - 50 = 10% overrun in cost is expected even if work efficiency can be increased to historical averages. If comparable cost overruns continue to accumulate, then the cost-to-complete will be even higher.

Figure 12-1 Illustration of Proportion Completion versus Expenditure for an Activity

Back to top

12.4 Financial Accounting Systems and Cost Accounts

The cost accounts described in the previous sections provide only one of the various components in a financial accounting system. Before further discussing the use of cost accounts in project control, the relationship of project and financial accounting deserves mention. Accounting information is generally used for three distinct purposes:

- Internal reporting to project managers for day-to-day planning, monitoring and control.

- Internal reporting to managers for aiding strategic planning.

- External reporting to owners, government, regulators and other outside parties.

External reports are constrained to particular forms and procedures by contractual reporting requirements or by generally accepted accounting practices. Preparation of such external reports is referred to as financial accounting. In contrast, cost or managerial accounting is intended to aid internal managers in their responsibilities of planning, monitoring and control.

Project costs are always included in the system of financial accounts associated with an organization. At the heart of this system, all expense transactions are recorded in a general ledger. The general ledger of accounts forms the basis for management reports on particular projects as well as the financial accounts for an entire organization. Other components of a financial accounting system include:

- The accounts payable journal is intended to provide records of bills received from vendors, material suppliers, subcontractors and other outside parties. Invoices of charges are recorded in this system as are checks issued in payment. Charges to individual cost accounts are relayed or posted to the General Ledger.

- Accounts receivable journals provide the opposite function to that of accounts payable. In this journal, billings to clients are recorded as well as receipts. Revenues received are relayed to the general ledger.

- Job cost ledgers summarize the charges associated with particular projects, arranged in the various cost accounts used for the project budget.

- Inventory records are maintained to identify the amount of materials available at any time.

In traditional bookkeeping systems, day to day transactions are first recorded in journals. With double-entry bookkeeping, each transaction is recorded as both a debit and a credit to particular accounts in the ledger. For example, payment of a supplier's bill represents a debit or increase to a project cost account and a credit or reduction to the company's cash account. Periodically, the transaction information is summarized and transferred to ledger accounts. This process is called posting, and may be done instantaneously or daily in computerized systems.

In reviewing accounting information, the concepts of flows and stocks should be kept in mind. Daily transactions typically reflect flows of dollar amounts entering or leaving the organization. Similarly, use or receipt of particular materials represent flows from or to inventory. An account balance represents the stock or cumulative amount of funds resulting from these daily flows. Information on both flows and stocks are needed to give an accurate view of an organization's state. In addition, forecasts of future changes are needed for effective management.

Information from the general ledger is assembled for the organization's financial reports, including balance sheets and income statements for each period. These reports are the basic products of the financial accounting process and are often used to assess the performance of an organization. Table12-5 shows a typical income statement for a small construction firm, indicating a net profit of $ 330,000 after taxes. This statement summarizes the flows of transactions within a year. Table 12-6 shows the comparable balance sheet, indicated a net increase in retained earnings equal to the net profit. The balance sheet reflects the effects of income flows during the year on the overall worth of the organization.

| Income Statement for the year ended December 31, 19xx | |

| Gross project revenues Direct project costs on contracts Operating Income | $7,200,000 5,500,000 6,500,000 700,000 150,000550,000 220,000 330,000 100,000 230,000 650,000 $880,000. |

| Balance Sheet December 31, 19xx | |

| Assets | Amount |

| Cash Payments Receivable Work in progress, not claimed Work in progress, retention Equipment at cost less accumulated depreciation Total assets | $150,000 750,000 700,000 200,000 1,400,000 $3,200,000 |

| Liabilities and Equity | |

| Liabilities Accounts payable Other items payable (taxes, wages, etc.) Long term debts Subtotal Shareholders' funds 40,000 shares of common stock (Including paid-in capital) Retained Earnings Subtotal Total Liabilities and Equity | $950,000 50,000 500,000 1,500,000 820,000 880,0001,700,000 $3,200,000 |

In the context of private construction firms, particular problems arise in the treatment of uncompleted contracts in financial reports. Under the "completed-contract" method, income is only reported for completed projects. Work on projects underway is only reported on the balance sheet, representing an asset if contract billings exceed costs or a liability if costs exceed billings. When a project is completed, the total net profit (or loss) is reported in the final period as income. Under the "percentage-of-completion" method, actual costs are reported on the income statement plus a proportion of all project revenues (or billings) equal to the proportion of work completed during the period. The proportion of work completed is computed as the ratio of costs incurred to date and the total estimated cost of the project. Thus, if twenty percent of a project was completed in a particular period at a direct cost of $180,000 and on a project with expected revenues of $1,000,000, then the contract revenues earned would be calculated as $1,000,000(0.2) = $200,000. This figure represents a profit and contribution to overhead of $200,000 - $180,000 = $20,000 for the period. Note that billings and actual receipts might be in excess or less than the calculated revenues of $200,000. On the balance sheet of an organization using the percentage-of-completion method, an asset is usually reported to reflect billings and the estimated or calculated earnings in excess of actual billings.

As another example of the difference in the "percentage-of-completion" and the "completed-contract" methods, consider a three year project to construct a plant with the following cash flow for a contractor:

| Year | Contract Expenses | Payments Received |

| 1 2 3 Total | $700,000 180,000 320,000 $1,200,000 | $900,000 250,000 150,000 $1,300,000 |

The supervising architect determines that 60% of the facility is complete in year 1 and 75% in year 2. Under the "percentage-of-completion" method, the net income in year 1 is $780,000 (60% of $1,300,000) less the $700,000 in expenses or $80,000. Under the "completed-contract" method, the entire profit of $100,000 would be reported in year 3.

The "percentage-of-completion" method of reporting period earnings has the advantage of representing the actual estimated earnings in each period. As a result, the income stream and resulting profits are less susceptible to precipitate swings on the completion of a project as can occur with the "completed contract method" of calculating income. However, the "percentage-of-completion" has the disadvantage of relying upon estimates which can be manipulated to obscure the actual position of a company or which are difficult to reproduce by outside observers. There are also subtleties such as the deferral of all calculated income from a project until a minimum threshold of the project is completed. As a result, interpretation of the income statement and balance sheet of a private organization is not always straightforward. Finally, there are tax disadvantages from using the "percentage-of-completion" method since corporate taxes on expected profits may become due during the project rather than being deferred until the project completion. As an example of tax implications of the two reporting methods, a study of forty-seven construction firms conducted by the General Accounting Office found that $280 million in taxes were deferred from 1980 to 1984 through use of the "completed-contract" method. [6]

It should be apparent that the "percentage-of-completion" accounting provides only a rough estimate of the actual profit or status of a project. Also, the "completed contract" method of accounting is entirely retrospective and provides no guidance for management. This is only one example of the types of allocations that are introduced to correspond to generally accepted accounting practices, yet may not further the cause of good project management. Another common example is the use of equipment depreciation schedules to allocate equipment purchase costs. Allocations of costs or revenues to particular periods within a project may cause severe changes in particular indicators, but have no real meaning for good management or profit over the entire course of a project. As Johnson and Kaplan argue: [7]

Today's management accounting information, driven by the procedures and cycle of the organization's financial reporting system, is too late, too aggregated and too distorted to be relevant for managers' planning and control decisions....

Management accounting reports are of little help to operating managers as they attempt to reduce costs and improve productivity. Frequently, the reports decrease productivity because they require operating managers to spend time attempting to understand and explain reported variances that have little to do with the economic and technological reality of their operations...

The managagement accounting system also fails to provide accurate product costs. Cost are distributed to products by simplistic and arbitrary measures, usually direct labor based, that do not represent the demands made by each product on the firm's resources.

As a result, complementary procedures to those used in traditional financial accounting are required to accomplish effective project control, as described in the preceding and following sections. While financial statements provide consistent and essential information on the condition of an entire organization, they need considerable interpretation and supplementation to be useful for project management.

Example 12-5: Calculating net profit

As an example of the calculation of net profit, suppose that a company began six jobs in a year, completing three jobs and having three jobs still underway at the end of the year. Details of the six jobs are shown in Table 12-7. What would be the company's net profit under, first, the "percentage-of-completion" and, second, the "completed contract method" accounting conventions?Back to top

TABLE 12-7 Example of Financial Records of Projects Net Profit on Completed Contracts (Amounts in thousands of dollars)

Job 2

Job 3

Total Net Profit on Completed Jobs

356

- 738

$1,054Status of Jobs Underway Job 4 Job 5 Job 6 Original Contract Price

Contract Changes (Change Orders, etc.)

Total Cost to Date

Payments Received or Due to Date

Estimated Cost to Complete$4,200

400

3,600

3,520

500$3,800

600

1,710

1,830

2,300$5,630

- 300

620

340

5,000As shown in Table 12-7, a net profit of $1,054,000 was earned on the three completed jobs. Under the "completed contract" method, this total would be total profit. Under the percentage-of completion method, the year's expected profit on the projects underway would be added to this amount. For job 4, the expected profits are calculated as follows:

Current contract price = Original contract price + Contract Changes

= 4,200 + 400 + 4,600Credit or debit to date = Total costs to date - Payments received or due to date

= 3,600 - 3,520 = - 80Contract value of uncompleted work = Current contract price - Payments received or due

= 4,600 - 3,520 = 1,080Credit or debit to come = Contract value of uncompleted work - Estimated Cost to Complete

= 1,080 - 500 = 580Estimated final gross profit = Credit or debit to date + Credit or debit to come

= - 80. + 580. = 500Estimated total project costs = Contract price - Gross profit

= 4,600 - 500 = 4,100Estimated Profit to date = Estimated final gross profit x Proportion of work complete

= 500. (3600/4100)) = 439Similar calculations for the other jobs underway indicate estimated profits to date of $166,000 for Job 5 and -$32,000 for Job 6. As a result, the net profit using the "percentage-of-completion" method would be $1,627,000 for the year. Note that this figure would be altered in the event of multi-year projects in which net profits on projects completed or underway in this year were claimed in earlier periods.

12.5 Control of Project Cash Flows

Section 12.3 described the development of information for the control of project costs with respect to the various functional activities appearing in the project budget. Project managers also are involved with assessment of the overall status of the project, including the status of activities, financing, payments and receipts. These various items comprise the project and financing cash flows described in earlier chapters. These components include costs incurred (as described above), billings and receipts for billings to owners (for contractors), payable amounts to suppliers and contractors, financing plan cash flows (for bonds or other financial instruments), etc.

As an example of cash flow control, consider the report shown in Table 12-8. In this case, costs are not divided into functional categories as in Table 12-4, such as labor, material, or equipment. Table 12-8 represents a summary of the project status as viewed from different components of the accounting system. Thus, the aggregation of different kinds of cost exposure or cost commitment shown in Table 12-0 has not been performed. The elements in Table 12-8 include:

- Costs

This is a summary of charges as reflected by the job cost accounts, including expenditures and estimated costs. This row provides an aggregate summary of the detailed activity cost information described in the previous section. For this example, the total costs as of July 2 (7/02) were $ 8,754,516, and the original cost estimate was $65,863,092, so the approximate percentage complete was 8,754,516/65,863,092 or 13.292%. However, the project manager now projects a cost of $66,545,263 for the project, representing an increase of $682,171 over the original estimate. This new estimate would reflect the actual percentage of work completed as well as other effects such as changes in unit prices for labor or materials. Needless to say, this increase in expected costs is not a welcome change to the project manager. - Billings

This row summarizes the state of cash flows with respect to the owner of the facility; this row would not be included for reports to owners. The contract amount was $67,511,602, and a total of $9,276,621 or 13.741% of the contract has been billed. The amount of allowable billing is specified under the terms of the contract between an owner and an engineering, architect, or constructor. In this case, total billings have exceeded the estimated project completion proportion. The final column includes the currently projected net earnings of $966,339. This figure is calculated as the contract amount less projected costs: 67,511,602 - 66,545,263 = $966,339. Note that this profit figure does not reflect the time value of money or discounting. - Payables

The Payables row summarizes the amount owed by the contractor to material suppliers, labor or sub-contractors. At the time of this report, $6,719,103 had been paid to subcontractors, material suppliers, and others. Invoices of $1,300,089 have accumulated but have not yet been paid. A retention of $391,671 has been imposed on subcontractors, and $343,653 in direct labor expenses have been occurred. The total of payables is equal to the total project expenses shown in the first row of costs. - Receivables

This row summarizes the cash flow of receipts from the owner. Note that the actual receipts from the owner may differ from the amounts billed due to delayed payments or retainage on the part of the owner. The net-billed equals the gross billed less retention by the owner. In this case, gross billed is $9,276,621 (as shown in the billings row), the net billed is $8,761,673 and the retention is $514,948. Unfortunately, only $7,209,344 has been received from the owner, so the open receivable amount is a (substantial!) $2,067,277 due from the owner. - Cash Position

This row summarizes the cash position of the project as if all expenses and receipts for the project were combined in a single account. The actual expenditures have been $7,062,756 (calculated as the total costs of $8,754,516 less subcontractor retentions of $391,671 and unpaid bills of $1,300,089) and $ 7,209,344 has been received from the owner. As a result, a net cash balance of $146,588 exists which can be used in an interest earning bank account or to finance deficits on other projects.

Each of the rows shown in Table 12-8 would be derived from different sets of financial accounts. Additional reports could be prepared on the financing cash flows for bonds or interest charges in an overdraft account.

| Costs 7/02 | Charges 8,754,516 | Estimated 65,863,092 | % Complete 13.292 | Projected 66,545,263 | Change 682,171 |

| Billings 7/01 | Contract 67,511,602 | Gross Bill 9,276,621 | % Billed 13.741 | Profit 966,339 | |

| Payables 7/01 | Paid 6,719,103 | Open 1,300,089 | Retention 391,671 | Labor 343,653 | Total 8,754,516 |

| Receivable 7/02 | Net Bill 8,761,673 | Received 7,209,344 | Retention 514,948 | Open 2,067,277 | |

| Cash Position | Paid 7,062,756 | Received 7,209,344 | Position 146,588 |

The overall status of the project requires synthesizing the different pieces of information summarized in Table 12-8. Each of the different accounting systems contributing to this table provides a different view of the status of the project. In this example, the budget information indicates that costs are higher than expected, which could be troubling. However, a profit is still expected for the project. A substantial amount of money is due from the owner, and this could turn out to be a problem if the owner continues to lag in payment. Finally, the positive cash position for the project is highly desirable since financing charges can be avoided.

The job status reports illustrated in this and the previous sections provide a primary tool for project cost control. Different reports with varying amounts of detail and item reports would be prepared for different individuals involved in a project. Reports to upper management would be summaries, reports to particular staff individuals would emphasize their responsibilities (eg. purchasing, payroll, etc.), and detailed reports would be provided to the individual project managers. Coupled with scheduling reports described in Chapter 10, these reports provide a snapshot view of how a project is doing. Of course, these schedule and cost reports would have to be tempered by the actual accomplishments and problems occurring in the field. For example, if work already completed is of sub-standard quality, these reports would not reveal such a problem. Even though the reports indicated a project on time and on budget, the possibility of re-work or inadequate facility performance due to quality problems would quickly reverse that rosy situation.

Back to top12.6 Schedule Control

In addition to cost control, project managers must also give considerable attention to monitoring schedules. Construction typically involves a deadline for work completion, so contractual agreements will force attention to schedules. More generally, delays in construction represent additional costs due to late facility occupancy or other factors. Just as costs incurred are compared to budgeted costs, actual activity durations may be compared to expected durations. In this process, forecasting the time to complete particular activities may be required.

The methods used for forecasting completion times of activities are directly analogous to those used for cost forecasting. For example, a typical estimating formula might be:

| (12.5) |  |

where Df is the forecast duration, W is the amount of work, and ht is the observed productivity to time t. As with cost control, it is important to devise efficient and cost effective methods for gathering information on actual project accomplishments. Generally, observations of work completed are made by inspectors and project managers and then work completed is estimated as described in Section 12.3. Once estimates of work complete and time expended on particular activities is available, deviations from the original duration estimate can be estimated. The calculations for making duration estimates are quite similar to those used in making cost estimates in Section 12.3.

For example, Figure 12-2 shows the originally scheduled project progress versus the actual progress on a project. This figure is constructed by summing up the percentage of each activity which is complete at different points in time; this summation can be weighted by the magnitude of effort associated with each activity. In Figure 12-2, the project was ahead of the original schedule for a period including point A, but is now late at point B by an amount equal to the horizontal distance between the planned progress and the actual progress observed to date.

Figure 12-2 Illustration of Planned versus Actual Progress over Time on a Project

Schedule adherence and the current status of a project can also be represented on geometric models of a facility. For example, an animation of the construction sequence can be shown on a computer screen, with different colors or other coding scheme indicating the type of activity underway on each component of the facility. Deviations from the planned schedule can also be portrayed by color coding. The result is a mechanism to both indicate work in progress and schedule adherence specific to individual components in the facility.

In evaluating schedule progress, it is important to bear in mind that some activities possess float or scheduling leeway, whereas delays in activities on the critical path will cause project delays. In particular, the delay in planned progress at time t may be soaked up in activities' float (thereby causing no overall delay in the project completion) or may cause a project delay. As a result of this ambiguity, it is preferable to update the project schedule to devise an accurate protrayal of the schedule adherence. After applying a scheduling algorithm, a new project schedule can be obtained. For cash flow planning purposes, a graph or report similar to that shown in Figure 12-3 can be constructed to compare actual expenditures to planned expenditures at any time. This process of re-scheduling to indicate the schedule adherence is only one of many instances in which schedule and budget updating may be appropriate, as discussed in the next section.

Figure 12-3 Illustration of Planned versus Actual Expenditures on a Project

Back to top

12.7 Schedule and Budget Updates

Scheduling and project planning is an activity that continues throughout the lifetime of a project. As changes or discrepancies between the plan and the realization occur, the project schedule and cost estimates should be modified and new schedules devised. Too often, the schedule is devised once by a planner in the central office, and then revisions or modifications are done incompletely or only sporadically. The result is the lack of effective project monitoring and the possibility of eventual chaos on the project site.

On "fast track" projects, initial construction activities are begun even before the facility design is finalized. In this case, special attention must be placed on the coordinated scheduling of design and construction activities. Even in projects for which the design is finalized before construction begins, change orders representing changes in the "final" design are often issued to incorporate changes desired by the owner.

Periodic updating of future activity durations and budgets is especially important to avoid excessive optimism in projects experiencing problems. If one type of activity experiences delays on a project, then related activities are also likely to be delayed unless managerial changes are made. Construction projects normally involve numerous activities which are closely related due to the use of similar materials, equipment, workers or site characteristics. Expected cost changes should also be propagated thoughout a project plan. In essence, duration and cost estimates for future activities should be revised in light of the actual experience on the job. Without this updating, project schedules slip more and more as time progresses. To perform this type of updating, project managers need access to original estimates and estimating assumptions.

Unfortunately, most project cost control and scheduling systems do not provide many aids for such updating. What is required is a means of identifying discrepancies, diagnosing the cause, forecasting the effect, and propagating this effect to all related activities. While these steps can be undertaken manually, computers aids to support interactive updating or even automatic updating would be helpful. [8]

Beyond the direct updating of activity durations and cost estimates, project managers should have mechanisms available for evaluating any type of schedule change. Updating activity duration estimations, changing scheduled start times, modifying the estimates of resources required for each activity, and even changing the project network logic (by inserting new activities or other changes) should all be easily accomplished. In effect, scheduling aids should be directly available to project managers. [9] Fortunately, local computers are commonly available on site for this purpose.

Example 12-6: Schedule Updates in a Small Project

As an example of the type of changes that might be required, consider the nine activity project described in Section 10.3 and appearing in Figure 12-4. Also, suppose that the project is four days underway, with the current activity schedule and progress as shown in Figure 12-5. A few problems or changes that might be encountered include the following:Back to top

- An underground waterline that was previously unknown was ruptured during the fifth day of the project. An extra day was required to replace the ruptured section, and another day will be required for clean-up. What is the impact on the project duration?

- To analyze this change with the critical path scheduling procedure, the manager has the options of (1) changing the expected duration of activity C, General Excavation, to the new expected duration of 10 days or (2) splitting activity C into two tasks (corresponding to the work done prior to the waterline break and that to be done after) and adding a new activity representing repair and clean-up from the waterline break. The second approach has the advantage that any delays to other activities (such as activities D and E) could also be indicated by precedence constraints.

- Assuming that no other activities are affected, the manager decides to increase the expected duration of activity C to 10 days. Since activity C is on the critical path, the project duration also increases by 2 days. Applying the critical path scheduling procedure would confirm this change and also give a new set of earliest and latest starting times for the various activities.

- After 8 days on the project, the owner asks that a new drain be installed in addition to the sewer line scheduled for activity G. The project manager determines that a new activity could be added to install the drain in parallel with Activity G and requiring 2 days. What is the effect on the schedule?

- Inserting a new activity in the project network between nodes 3 and 4 violates the activity-on-branch convention that only one activity can be defined between any two nodes. Hence, a new node and a dummy activity must be inserted in addition to the drain installation activity. As a result, the nodes must be re-numbered and the critical path schedule developed again. Performing these operations reveals that no change in the project duration would occur and the new activity has a total float of 1 day.

- To avoid the labor associated with modifying the network and re-numbering nodes, suppose that the project manager simply re-defined activity G as installation of sewer and drain lines requiring 4 days. In this case, activity G would appear on the critical path and the project duration would increase. Adding an additional crew so that the two installations could proceed in parallel might reduce the duration of activity G back to 2 days and thereby avoid the increase in the project duration.

- At day 12 of the project, the excavated trenches collapse during Activity E. An additional 5 days will be required for this activity. What is the effect on the project schedule? What changes should be made to insure meeting the completion deadline?

- Activity E has a total float of only 1 day. With the change in this activity's duration, it will lie on the critical path and the project duration will increase.

- Analysis of possible time savings in subsequent activities is now required, using the procedures described in Section 10.9.

Figure 12-4 A Nine Activity Example Project

Figure 12-5 Current Schedule for an Example Project Presented as a Bar Chart

As can be imagined, it is not at all uncommon to encounter changes during the course of a project that require modification of durations, changes in the network logic of precedence relationships, or additions and deletions of activities. Consequently, the scheduling process should be readily available as the project is underway.

12.8 Relating Cost and Schedule Information

The previous sections focused upon the identification of the budgetary and schedule status of projects. Actual projects involve a complex inter-relationship between time and cost. As projects proceed, delays influence costs and budgetary problems may in turn require adjustments to activity schedules. Trade-offs between time and costs were discussed in Section 10.9 in the context of project planning in which additional resources applied to a project activity might result in a shorter duration but higher costs. Unanticipated events might result in increases in both time and cost to complete an activity. For example, excavation problems may easily lead to much lower than anticipated productivity on activities requiring digging.

While project managers implicitly recognize the inter-play between time and cost on projects, it is rare to find effective project control systems which include both elements. Usually, project costs and schedules are recorded and reported by separate application programs. Project managers must then perform the tedious task of relating the two sets of information.

The difficulty of integrating schedule and cost information stems primarily from the level of detail required for effective integration. Usually, a single project activity will involve numerous cost account categories. For example, an activity for the preparation of a foundation would involve laborers, cement workers, concrete forms, concrete, reinforcement, transportation of materials and other resources. Even a more disaggregated activity definition such as erection of foundation forms would involve numerous resources such as forms, nails, carpenters, laborers, and material transportation. Again, different cost accounts would normally be used to record these various resources. Similarly, numerous activities might involve expenses associated with particular cost accounts. For example, a particular material such as standard piping might be used in numerous different schedule activities. To integrate cost and schedule information, the disaggregated charges for specific activities and specific cost accounts must be the basis of analysis.

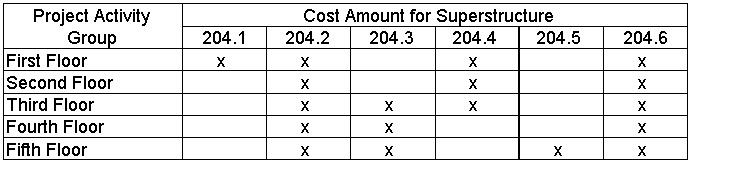

A straightforward means of relating time and cost information is to define individual work elements representing the resources in a particular cost category associated with a particular project activity. Work elements would represent an element in a two-dimensional matrix of activities and cost accounts as illustrated in Figure 12-6. A numbering or identifying system for work elements would include both the relevant cost account and the associated activity. In some cases, it might also be desirable to identify work elements by the responsible organization or individual. In this case, a three dimensional representation of work elements is required, with the third dimension corresponding to responsible individuals. [10] More generally, modern computerized databases can accomadate a flexible structure of data representation to support aggregation with respect to numerous different perspectives; this type of system will be discussed in Chapter 14.

With this organization of information, a number of management reports or views could be generated. In particular, the costs associated with specific activities could be obtained as the sum of the work elements appearing in any row in Figure 12-6. These costs could be used to evaluate alternate technologies to accomplish particular activities or to derive the expected project cash flow over time as the schedule changes. From a management perspective, problems developing from particular activities could be rapidly identified since costs would be accumulated at such a disaggregated level. As a result, project control becomes at once more precise and detailed.

Figure 12-6 Illustration of a Cost Account and Project Activity Matrix

Unfortunately, the development and maintenance of a work element database can represent a large data collection and organization effort. As noted earlier, four hundred separate cost accounts and four hundred activities would not be unusual for a construction project. The result would be up to 400x400 = 160,000 separate work elements. Of course, not all activities involve each cost account. However, even a density of two percent (so that each activity would have eight cost accounts and each account would have eight associated activities on the average) would involve nearly thirteen thousand work elements. Initially preparing this database represents a considerable burden, but it is also the case that project bookkeepers must record project events within each of these various work elements. Implementations of the "work element" project control systems have typically fondered on the burden of data collection, storage and book-keeping.

Until data collection is better automated, the use of work elements to control activities in large projects is likely to be difficult to implement. However, certain segments of project activities can profit tremendously from this type of organization. In particular, material requirements can be tracked in this fashion. Materials involve only a subset of all cost accounts and project activities, so the burden of data collection and control is much smaller than for an entire system. Moreover, the benefits from integration of schedule and cost information are particularly noticeable in materials control since delivery schedules are directly affected and bulk order discounts might be identified. Consequently, materials control systems can reasonably encompass a "work element" accounting system.

In the absence of a work element accounting system, costs associated with particular activities are usually estimated by summing expenses in all cost accounts directly related to an activity plus a proportion of expenses in cost accounts used jointly by two or more activities. The basis of cost allocation would typically be the level of effort or resource required by the different activities. For example, costs associated with supervision might be allocated to different concreting activities on the basis of the amount of work (measured in cubic yards of concrete) in the different activities. With these allocations, cost estimates for particular work activities can be obtained.

Back to top12.9 References

- American Society of Civil Engineers, "Construction Cost Control," ASCE Manuals and Reports of Engineering Practice No. 65, Rev. Ed., 1985.

- Coombs, W.E. and W.J. Palmer, Construction Accounting and Financial Management, McGraw-Hill, New York, 1977.

- Halpin, D. W., Financial and Cost Concepts for Construction Management, John Wiley & Sons, New York, 1985.

- Johnson, H. Thomas and Robert S. Kaplan, Relevance Lost, The Rise and Fall of Management Accounting, Harvard Business School Press, Boston, MA 1987.

- Mueller, F.W. Integrated Cost and Schedule Control for Construction Projects, Van Nostrand Reinhold Company, New York, 1986.

- Tersine, R.J., Principles of Inventory and Materials Management, North Holland, 1982.

12.10 Problems

- Suppose that the expected expenditure of funds in a particular category was expected to behave in a piecewise linear fashion over the course of the project. In particular, the following points have been established from historical records for the percentage of completion versus the expected expenditure (as a percentage of the budget):

Percentage of Completion Expected Expenditure 0%

20%

40%

60%

80%

100%0%

10%

25%

55%

90%

100%a. Graph the relationship between percentage complete and expected expenditure.

b. Develop a formula or set of formulas for forecasting the ultimate expenditure on this activity given the percentage of completion. Assume that any over or under expenditure will continue to grow proportionately during the course of the project.

c. Using your formula, what is the expected expenditure as a percentage of the activity budget if:

i. 15% of funds have been expended and 15% of the activity is complete.

ii. 30% of funds have been expended and 30% of the activity is complete.

iii. 80% of funds have been expended and 80% of the activity is complete. - Repeat Problem 1 parts (b) and (c) assuming that any over or under expenditure will not continue to grow during the course of the project.

- Suppose that you have been asked to take over as project manager on a small project involving installation of 5,000 linear feet (LF) of metal ductwork in a building. The job was originally estimated to take ten weeks, and you are assuming your duties after three weeks on the project. The original estimate assumed that each linear foot of ductwork would cost $10, representing $6 in labor costs and $4 in material cost. The expected production rate was 500 linear feet of ductwork per week. Appearing below is the data concerning this project available from your firm's job control information system:

Week Weekly Unit Costs ($/Lf)

Quantity Placed (Lf)

Total Cost

Labor Materials Total Week To Date Week To Date 1

2

312.00

8.57

6.674.00

4.00

4.0016.00

12.57

10.67250

350

450250

600

1,0504,000

4,400

4,8004,000

8,400

13,200a. Based on an extrapolation using the average productivity and cost for all three weeks, forecast the completion time, cost and variance from original estimates.

b. Suppose that you assume that the productivity achieved in week 3 would continue for the remainder of the project. How would this affect your forecasts in (a)? Prepare new forecasts based on this assumption. - What criticisms could you make of the job status report in the previous problem from the viewpoint of good project management?

- Suppose that the following estimate was made for excavation of 120,000 cubic yards on a site:

Resource

Quantity

Cost

Machines

Labor

Trucks

Total 1,200 hours

6,000 hours

2,400 hours

$60,000

150,000

75,000

$285,000After 95,000 cubic yards of excavation was completed, the following expenditures had been recorded:

Resource

Quantity

Cost

Machines

Labor

Trucks

Total 1,063 hours

7,138 hours

1,500 hours

$47,835

142,527

46,875

$237,237a. Calculate estimated and experienced productivity (cubic yards per hour) and unit cost (cost per cubic yard) for each resource.

b. Based on straight line extrapolation, do you see any problem with this activity? If so, can you suggest a reason for the problem based on your findings in (a)? - Suppose the following costs and units of work completed were recorded on an activity:

Month Monthly

ExpenditureNumber of

Work Units Completed1

2

3

4

5

6$1,200

$1,250

$1,260

$1,280

$1,290

$1,28030

32

38

42

42

42Answer the following questions:

a. For each month, determine the cumulative cost, the cumulative work completed, the average cumulative cost per unit of work, and the monthly cost per unit of work.

b. For each month, prepare a forecast of the eventual cost-to-complete the activity based on the proportion of work completed.

c. For each month, prepare a forecast of the eventual cost-to-complete the activity based on the average productivity experienced on the activity.

d. For each month, prepare a forecast of the eventual cost-to-complete the activity based on the productivity experienced in the previous month.

e. Which forecasting method (b, c or d) is preferable for this activity? Why? - Repeat Problem 6 for the following expenditure pattern:

Month Monthly

ExpenditureNumber of

Work Units Completed1

2

3

4

5

6$1,200

$1,250

$1,260

$1,280

$1,290

$1,30030

35

45

48

52

54 - Why is it difficult to integrate scheduling and cost accounting information in project records?

- Prepare a schedule progress report on planned versus actual expenditure on a project (similar to that in Figure 12-5) for the project described in Example 12-6.

- Suppose that the following ten activities were agreed upon in a contract between an owner and an engineer.

Original Work Plan Information Activity Duration (months) Predecessors Estimated Cost ($ thousands) A

B

C

D

E

F

G

H

I

J2

5

5

2

3

8

4

4

11

2---

---

B

C

B

---

E, F

E, F

B

E, F7

9

8

4

1

7

6

5

10

7Original Contract Information Total Direct Cost

Overhead

Total Direct and Overhead

Profit

Total Contract Amount$64

64

128

12.8

$140.8First Year Cash Flow Expenditures

Receipts$56,000

$60,800The markup on the activities' costs included 100% overhead and a profit of 10% on all costs (including overhead). This job was suspended for one year after completion of the first four activities, and the owner paid a total of $60,800 to the engineer. Now the owner wishes to re-commence the job. However, general inflation has increased costs by ten percent in the intervening year. The engineer's discount rate is 15 percent per year (in current year dollars). For simplicity, you may assume that all cash transactions occur at the end of the year in making discounting calculations in answering the following questions:

a. How long will be remaining six activities require?

b. Suppose that the owner agrees to make a lump sum payment of the remaining original contract at the completion of the project. Would the engineer still make a profit on the job? If so, how much?

c. Given that the engineer would receive a lump sum payment at the end of the project, what amount should he request in order to earn his desired ten percent profit on all costs?

d. What is the net future value of the entire project at the end, assuming that the lump sum payment you calculated in (c) is obtained? - Based on your knowledge of coding systems such as MASTERFORMAT and estimating techniques, outline the procedures that might be implemented to accomplish:

a. automated updating of duration and cost estimates of activities in light of experience on earlier, similar activities.

b. interactive computer based aids to help a project manager to accomplish the same task.

12.11 Footnotes

1. Cited in Zoll, Peter F., "Database Structures for Project Management," Proceedings of the Seventh Conference on Electronic Computation, ASCE, 1979. Back

2. Thomas Gibb reports a median number of 400 cost accounts for a two-million dollar projects in a sample of 30 contractors in 1975. See T.W. Gibb, Jr., "Building Construction in Southeastern United States," School of Civil Engineering, Georgia Institute of Technology, 1975, reported in D.W. Halpin, Financial and Cost Concepts for Construction Management, John Wiley and Sons, 1985. Back

3. This illustrative set of accounts was adapted from an ASCE Manual of Practice: Construction Cost Control, Task Committee on Revision of Construction Cost Control Manual, ASCE, New York, 1985. Back

4. For a fuller exposition of this point, see W.H. Lucas and T.L. Morrison, "Management Accounting for Construction Contracts," Management Accounting, 1981, pp. 59-65. Back

5. For a description of these methods and examples as used by a sample of construction companies, see L.S. Riggs, Cost and Schedule Control in Industrial Construction, Report to The Construction Industry Institute, Dec. 1986. Back

6. As reported in the Wall Street Journal, Feb. 19, 1986, pg. A1, c. 4. Back

7. H.T. Johnson and R.S. Kaplan, Relevance Lost, The Rise and Fall of Management Accounting, Harvard Business School Press, pg. 1, 1987. Back

8. One experimental program directed at this problem is a knowledge based expert system described in R.E. Levitt and J.C. Kunz, "Using Knowledge of Construction and Project Management for Automated Schedule Updating," Project Management Journal, Vol. 16, 1985, pp. 57-76. Back

9. For an example of a prototype interactive project management environment that includes graphical displays and scheduling algorithms, see R. Kromer, "Interactive Activity Network Analysis Using a Personal Computer," Unpublished MS Thesis, Department of Civil Engineering, Carnegie-Mellon University, Pittsburgh, PA, 1984. Back

10. A three dimensional work element definition was proposed by J.M. Neil, "A System for Integrated Project Management," Proceedings of the Conference on Current Practice in Cost Estimating and Cost Control, ASCE, Austin, Texas, 138-146, April 1983. Back

| Previous Chapter | | | Table of Contents | | | Next Chapter |

Construction Accounting and Financial Management Chapter 3 Solutions

Source: https://www.cmu.edu/cee/projects/PMbook/12_Cost_Control,_Monitoring,_and_Accounting.html